The Institute of Chartered Accountants of India (ICAI) has announced a significant one-year postponement for the implementation of the fourth phase of its mandatory Peer Review system. This move offers a crucial window of preparation for numerous chartered accountancy firms across the country.

Revised Timeline and Official Announcement

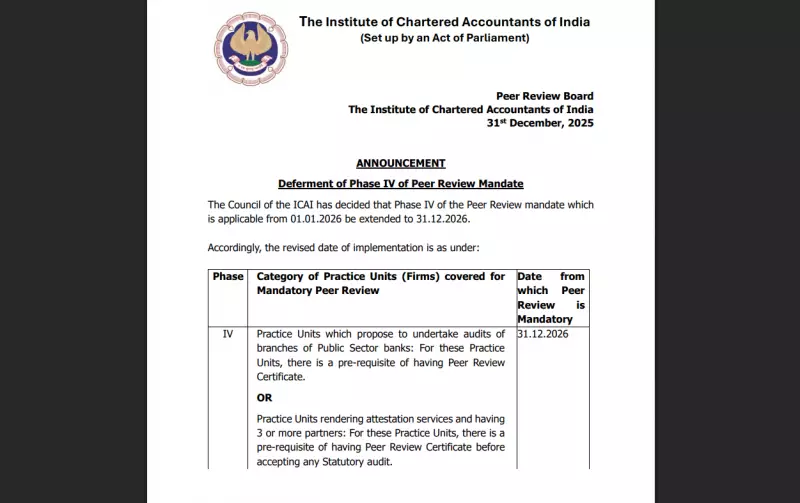

In an official notice released on December 31, 2025, the ICAI Peer Review Board communicated the Council's decision to defer Phase IV. The new implementation date is now December 31, 2026, shifting from the originally scheduled January 1, 2026. This uniform extension applies to all practice units falling under the ambit of this phase.

The deferral is seen as a strategic step by the accounting regulator to allow firms additional time for readiness and smoother integration with the peer review framework. The existing peer review system for earlier phases continues to operate unchanged until the revised deadline.

What Phase IV Covers and Why the Delay Matters

Phase IV of the Peer Review Mandate specifically targets two key categories of practice units:

- Firms that propose to undertake audits of branches of Public Sector banks. For them, a valid Peer Review Certificate is a mandatory pre-condition.

- Practice units that provide attestation services and have three or more partners. These firms must obtain the certificate before accepting any statutory audit assignment.

The one-year extension provides temporary relief, especially for small and mid-sized firms. The peer review process is comprehensive, involving meticulous documentation, internal system checks, and interactions with reviewers. The extra time alleviates immediate pressure, enabling firms to plan and execute their compliance in a structured manner without risking professional disqualification.

Implications and Next Steps for CA Firms

While the deadline has been pushed back, the ICAI has made it clear that the requirement itself has not been relaxed. The extension merely shifts the compliance deadline. Firms targeting Public Sector bank audits or multi-partner firms expanding their statutory audit work must still obtain the necessary Peer Review Certificate before the new effective date of December 31, 2026, to remain eligible.

The ICAI has advised all concerned practice units to utilize this extended period effectively. Initiating the peer review process well in advance is critical to avoid a last-minute rush and ensure uninterrupted professional practice once the mandate is enforced. The deferment serves as a clear signal for firms to begin their preparations early, turning the breathing space into an opportunity for robust compliance.