Telangana Survey Exposes Stark Urban Credit Divide and Moneylender Dependence

The Telangana Socio-Economic, Educational, Employment, Political and Caste (SEEEPC) Survey-2024 has uncovered a concerning urban credit divide across the state, revealing that numerous towns and district headquarters remain heavily reliant on moneylenders despite their position outside the traditional rural economy. This finding challenges the assumption that urban residence automatically translates to financial inclusion and access to formal banking systems.

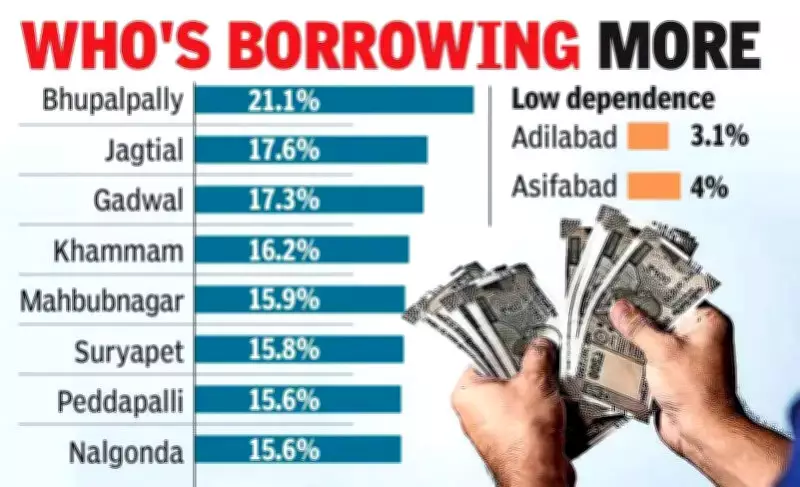

Sharp Disparities in Urban Borrowing Patterns

While only 3.6% of urban households across Telangana reported borrowing from moneylenders, this figure masks dramatic variations at the district level. The survey data exposes deep gaps in access to institutional finance, with several districts showing significantly higher dependence on informal lenders. This uneven spread of formal financial services highlights a clear development imbalance within urban areas of the state.

Jayashankar Bhupalpally recorded the highest share of urban households taking loans from moneylenders at 21.1%, which is nearly six times the state urban average. Following closely were Jagtial at 17.6%, Jogulamba Gadwal at 17.3%, Khammam at 16.2%, Mahbubnagar at 15.9%, Suryapet at 15.8%, and both Peddapalli and Nalgonda at 15.6% each.

In stark contrast, districts such as Adilabad at 3.1% and Kumuram Bheem Asifabad at 4% reported much lower levels of moneylender dependence. This sharp contrast suggests that smaller towns face far greater reliance on informal lenders compared to better-served urban centers like Hyderabad.

Persistent Caste Disparities in Urban Credit Access

The survey also revealed strong caste-based disparities within urban areas, indicating that financial exclusion persists along social lines. Scheduled Castes (SCs) and Scheduled Tribes (STs) frequently reported the highest dependence on moneylenders, demonstrating that urban residence alone has not bridged the financial inclusion gap.

In Jagtial, 29.2% of urban ST households and 20.4% of SC households reported taking loans from moneylenders, compared with just 9.6% among Other Castes (OCs). Similarly, in Bhupalpally, SC households showed the highest dependence at 25.5%, followed by ST households at 23.9%, while OCs stood at 10.1%.

The pattern varied across districts but consistently showed higher vulnerability among marginalized communities. In Peddapalli, both SC and ST households reported 19.2% dependence, far above the 7.4% among OCs. In Gadwal, ST households stood at 23.4%, while in Khammam, dependence was more evenly spread across communities with 17% among STs, 14.9% among SCs, 16.5% among Backward Classes (BCs), and 16.3% among OCs.

Statewide Implications and Financial Exclusion

Statewide, 6.8% of all households reported loans from moneylenders, with the share significantly higher among marginalized communities: 9.7% among STs, 8.8% among SCs, 7.1% among BCs, and 5.1% among OCs. The survey directly links this trend to exclusion from formal lending systems, suggesting that despite overall lower credit stress in urban Telangana compared to rural areas, several district towns continue to rely substantially on private lenders who typically charge higher interest rates.

The findings underscore that the spread of formal finance across urban Telangana remains highly uneven, with smaller towns facing greater financial vulnerability. Districts like Jagtial stand out as stark examples, where 17.6% of urban households reported borrowing from moneylenders—nearly five times the state urban average. Bhupalpally was even higher at 21.1%, while Peddapalli stood at 15.6%.

Other districts including Khammam, Nalgonda, Suryapet, Mahbubnagar, and Gadwal also remained in this elevated range, demonstrating that the problem cuts across geographical regions. The survey highlights that urban residence does not automatically guarantee access to formal credit, particularly for marginalized communities living in smaller towns.

This comprehensive data from the SEEEPC Survey-2024 provides crucial insights into the persistent challenges of financial inclusion in urban Telangana, revealing both geographical and social dimensions of credit access disparities that require targeted policy interventions.