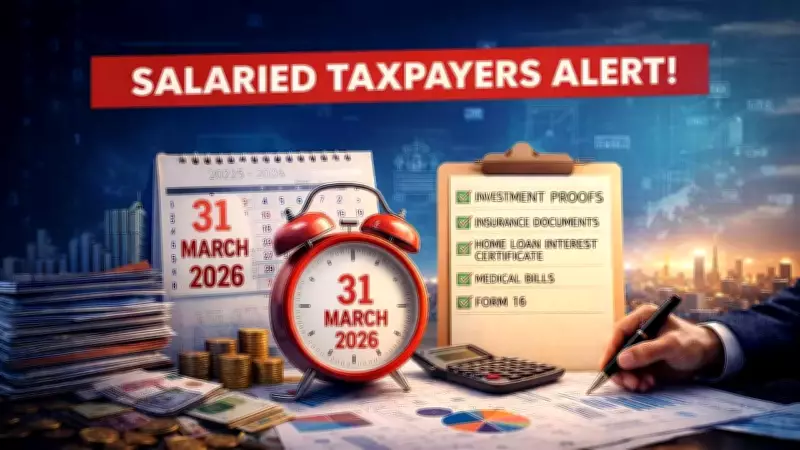

Strategic Year-End Tax Planning for Salaried Indians: Navigating Deadlines and Regimes

As the financial year draws to a close, millions of salaried taxpayers across India enter a critical and decisive phase. What was once a routine process of submitting investment proofs to employers has now evolved into a highly strategic endeavor. Year-end tax planning today directly impacts your take-home salary, refund timelines, and the likelihood of receiving automated notices from the Income Tax Department. With March 31, 2026, serving as the definitive cut-off, only investments and expenditures completed on or before this date qualify for tax benefits for the financial year 2025-26.

Understanding the Two Tax Regimes: Old vs. New

India currently offers two parallel tax systems for individuals: the Old Personal Tax Regime and the New Personal Tax Regime. While the new regime is now the default option, the choice remains with the taxpayer. The old tax regime benefits those with significant deductible expenses and structured investments, allowing deductions for items like Life Insurance, Equity Linked Savings Schemes (ELSS), Public Provident Fund (PPF) contributions, Health Insurance premiums, House Rent Allowance (HRA), Leave Travel Allowance (LTA), and home loan interest deductions. It provides a Rs 50,000 standard deduction and a rebate up to Rs 5 lakhs, but requires meticulous record-keeping due to higher slab rates.

In contrast, the new regime offers lower slab rates, an increased standard deduction of Rs 75,000, and a full tax rebate for income up to Rs 12 lakh. It removes most exemptions and deductions, simplifying compliance. According to recent data from the Income Tax Department, 88% of individual taxpayers have opted for the new regime. The optimal choice depends entirely on your income level and eligible deductions, with no universal "better" option. Using the Government’s online tax calculator can help compare both regimes effectively.

The Critical Role of Documentation and Deadlines

For those opting for the old regime, documentation is not optional—it is critical. Every deduction claimed must be backed by valid documentary evidence, as employers rely on proofs submitted by employees, and the Income Tax Department cross-verifies claims through third-party reporting. Incomplete records can lead to disallowance of deductions, additional tax, and interest liability. Investment deadlines are non-negotiable; only transactions completed by March 31, 2026, qualify, so ensure payments are fully processed and acknowledged before the deadline to avoid lost deductions.

Employer Responsibilities and TDS Adjustments

Employers play a significant role in year-end tax outcomes. During March, companies conduct final TDS adjustments based on the tax regime selected, investment proofs submitted, and other income declared by the employee. If supporting documents are not submitted on time, employers must compute tax without considering exemptions, often leading to higher TDS deductions and lower take-home pay in the final month. Excess tax may remain locked until refund processing, which can take months. Employees should also declare income from other sources, such as bank interest or dividends, to ensure accurate TDS computation.

Overlooked Compliance: TDS on Rent

One frequently missed obligation involves tax withholding on high-value rent payments. If monthly rent exceeds Rs 50,000, tenants must deduct TDS at 2%, even if they are salaried individuals with no business income. Rules vary based on the landlord’s residential status: for residents, TDS is deducted once per financial year, typically in March; for non-residents, it must be deducted at each payment, at a higher rate of 30% plus surcharge and cess unless a lower certificate is obtained. Failure to comply can attract interest, late fees, and penalties, with automated systems now identifying such gaps.

Flexibility in Tax Regime Selection

A widespread misconception is that the tax regime chosen with the employer is final. However, salaried taxpayers may switch regimes when filing their Income Tax Return, provided it is done within the prescribed due date. Filing a belated return may restrict this option, offering relief to those who miscalculated their optimal regime earlier in the year.

The Era of Automated Scrutiny and Digital Reconciliation

India’s tax administration has shifted to a data-driven era, with the Income Tax Department cross-verifying income and deductions using Form No. 16, Form No. 26AS, Annual Information Statement (AIS), and Taxpayer Information Summary (TIS). Any mismatch can trigger automated notices, common triggers include HRA claims without rent income reflected, unreported bank interest, or Section 80C claims not matching investment reports. Taxpayers should periodically review these digital records to reconcile discrepancies before filing returns, as compliance is now a continuous, year-round responsibility.

In summary, year-end tax planning for salaried Indians is not merely about reducing liability—it is about ensuring seamless compliance in a system designed to validate every claim through accuracy, documentation, and timely action.