Income Tax Authorities Attach 4.4 Acres in Hyderabad Over Suspected Benami Land Transaction

In a significant enforcement action, the Income Tax Department has provisionally attached 4.4 acres of agricultural land located in Gajularamaram, Hyderabad. This move follows an attachment order that alleges five individuals with relatively modest disclosed incomes were acting as benamidars in a land deal valued at a staggering Rs 23.4 crore. The order suggests the transaction was prima facie funded by an unknown or fictitious beneficial owner.

Details of the Land Purchase and Subsequent Agreement

The attachment order details that the land was purchased through a sale deed dated December 28, 2023. The purchasers named in the document are:

- Chilukuri Venkata Rami Reddy

- K Narsimha Raj Goud

- S Munagala Sridhar

- Dyavanapally Shylender

- Maloth Venkatesh Naik

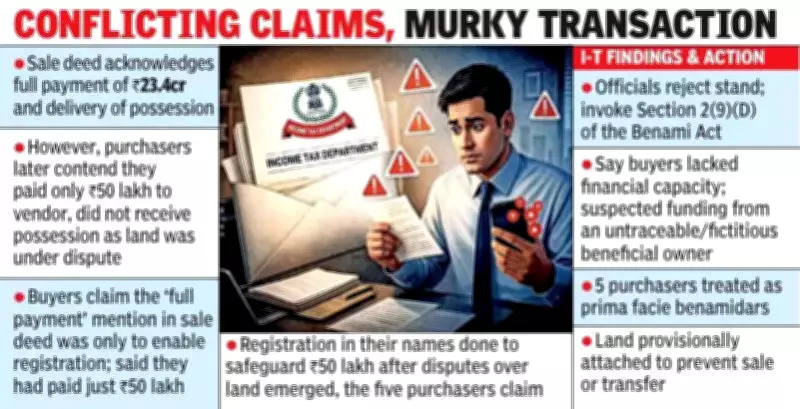

The stated consideration in the sale deed was Rs 23,46,75,870, which translates to approximately Rs 23.46 crore. Crucially, the entire amount was recorded as having been paid in cash, with possession of the land also noted as having been handed over to the purchasers.

However, the plot thickened when the Income Tax Department discovered that the same land was subsequently lined up for sale to the Koneru Lakshmaiah Education Foundation (KLU/KLEF) for an increased sum of Rs 30 crore. An advance payment of Rs 17 crore had already been received by the five purchasers from the educational foundation. This development prompted the tax authorities to intervene to prevent any further transfer of the property.

Scrutiny of Purchasers' Financial Profiles

The initiating officer's order highlights a critical discrepancy. Upon scrutiny, the annual incomes of the five named purchasers, as reflected in their income tax returns, were found to be insignificant when compared to the massive transaction value of Rs 23.46 crore. Based on this analysis, the officer concluded that these individuals lacked the necessary creditworthiness to fund such a large-scale cash purchase independently.

The order further notes that the original owner and vendor of the land was identified as Vakiti Sudhakar. Authorities summoned Sudhakar to provide a statement, but he did not appear before them.

Conflicting Claims Emerge During Investigation

A central finding in the provisional attachment order revolves around contradictory statements made by the purchasers. While the registered sale deed explicitly acknowledged full cash payment and delivery of possession, the five men later presented a different narrative to the authorities.

They contended that they had actually paid only Rs 50 lakh to the vendor, Vakiti Sudhakar, and had not received possession because the land was already embroiled in a dispute. They claimed the recital in the sale deed regarding full payment was included merely to facilitate the registration process, despite the entire amount not being paid.

The purchasers explained that they proceeded with registering the land in their names to safeguard the Rs 50 lakh they had already invested after disputes surfaced. Their stated plan was to sell the property to Koneru Lakshmaiah Education Foundation for Rs 30 crore, use those proceeds to pay the remaining balance to the original owner, and retain the difference as profit.

They maintained that the Rs 50 lakh part-payment came from legitimate, accounted sources visible in their income tax returns. They also argued that, had the land not been under dispute, they would have arranged the remaining funds through borrowings from banks or Non-Banking Financial Companies (NBFCs). According to their submission, Vakiti Sudhakar was unable to refund the initial Rs 50 lakh and had even issued legal notices seeking cancellation of the transaction due to his inability to complete the sale.

Provisional Attachment Ordered to Prevent Alienation

The initiating officer did not accept the explanation provided by the five purchasers. The order held that the transaction fell within the ambit of Section 2(9)(D) of the Prohibition of Benami Property Transactions Act, 1988.

The reasoning was clear: if the consideration mentioned in the sale deed (Rs 23.46 crore) was to be treated as paid, it evidently was not paid by the named purchasers given their financial profiles. Therefore, the funds must have originated from a non-traceable or fictitious beneficial owner. On this basis, the five individuals were treated as prima facie benamidars (name-lenders), while the actual source of the funds was attributed to an unknown beneficial owner whose identity remains unestablished.

To prevent the land from being sold, transferred, or otherwise alienated during the ongoing proceedings, the Initiating Officer passed a provisional attachment order on March 25, 2026. This action effectively freezes the property, safeguarding it as the investigation into the true source of the funds and the nature of the transaction continues.