Surat's Gem and Jewellery Sector Shows Signs of Stabilization in FY 2025-26

The gem and jewellery (GJ) sector in Surat, India's diamond polishing hub, demonstrated encouraging signs of stabilization during the 2025-26 financial year. After experiencing sharper declines over the previous two years, annual exports fell by only 3%, indicating a potential recovery trajectory for this critical industry.

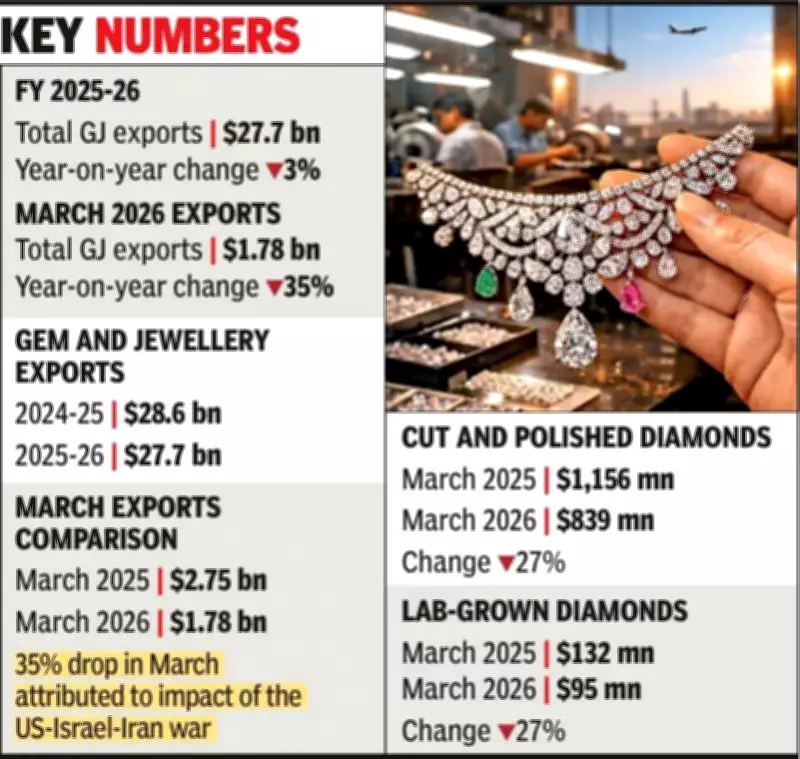

Overall Export Performance and March Concerns

Total GJ exports reached $27.7 billion during FY 2025-26, representing a modest decline from $28.6 billion recorded in the previous fiscal year. This relatively small contraction suggests the sector is beginning to find its footing after more significant challenges.

However, March performance has emerged as a substantial concern for industry stakeholders. Gross GJ exports plummeted by 35% in March 2026 compared to the same month last year, dropping sharply from $2.75 billion to $1.78 billion. Industry analysts attribute this dramatic decline primarily to the disruptive impact of the ongoing Iran war, which has created uncertainty in key markets and disrupted trade flows.

Diamond Segment Analysis

The diamond segment presented a mixed picture throughout the fiscal year. Gross exports of cut and polished diamonds (CPD) declined by 8%, falling from $13.29 billion in FY 2024-25 to $12.15 billion in the most recent fiscal year. This contraction reflects continued challenges in the global diamond market.

The March figures were particularly concerning for diamond exports. CPD exports during the month declined by 27%, dropping from $1,156 million in March 2025 to $839 million in March 2026. Polished lab-grown diamond (LGD) exports mirrored this trend with an identical 27% decline, falling from $132 million to $95 million over the same one-month period.

For the entire fiscal year, polished LGD exports totaled $1.13 billion, approximately 10% lower than the $1.26 billion recorded in the previous fiscal period. On the import side, gross imports of rough diamonds declined by 2%, decreasing from $10.76 billion to $10.47 billion, reflecting cautious buying behavior amid persistent global economic uncertainty.

Gold Jewellery Performance

Gold jewellery exports remained remarkably stable at $11.36 billion, showing virtually no change from the previous year's performance. This stability masks divergent trends within the gold jewellery category.

Plain gold jewellery exports declined by 7%, falling from $5.23 billion in FY 2024-25 to $4.84 billion in FY 2025-26. In contrast, studded gold jewellery exports demonstrated resilience with 6% growth, increasing from $6.12 billion to $6.52 billion over the same period.

Strong Growth in Other Precious Metals

While some segments faced challenges, other precious metal categories showed impressive expansion. Silver jewellery exports surged by an impressive 52%, climbing from $964 million in FY 2024-25 to $1,467 million in FY 2025-26. This remarkable growth indicates shifting consumer preferences and expanding market opportunities for silver products.

Platinum jewellery exports also experienced substantial growth, increasing by 39% from $183 million to $255 million over the same fiscal period. These strong performances in alternative precious metals suggest diversification within the broader jewellery sector.

Industry Outlook and Challenges

The 3% overall decline in GJ exports represents a significant improvement compared to the more severe contractions experienced in recent years. This stabilization suggests that adaptation strategies and market adjustments may be taking effect within the industry.

Nevertheless, the dramatic 35% export drop in March serves as a stark reminder of the sector's vulnerability to geopolitical events. The Iran war's impact on March exports highlights how international conflicts can rapidly disrupt trade patterns and consumer confidence in luxury goods markets.

Industry observers will be closely monitoring whether the March downturn represents a temporary setback or the beginning of a more challenging period. The mixed performance across different jewellery categories indicates that consumer preferences continue to evolve, with some traditional segments facing pressure while alternative materials gain market share.

As the gem and jewellery sector navigates these complex dynamics, the relatively modest annual decline offers cautious optimism for stakeholders in Surat and throughout India's jewellery manufacturing ecosystem.